Market Misjudgment and the Data’s Warning (The Gap)

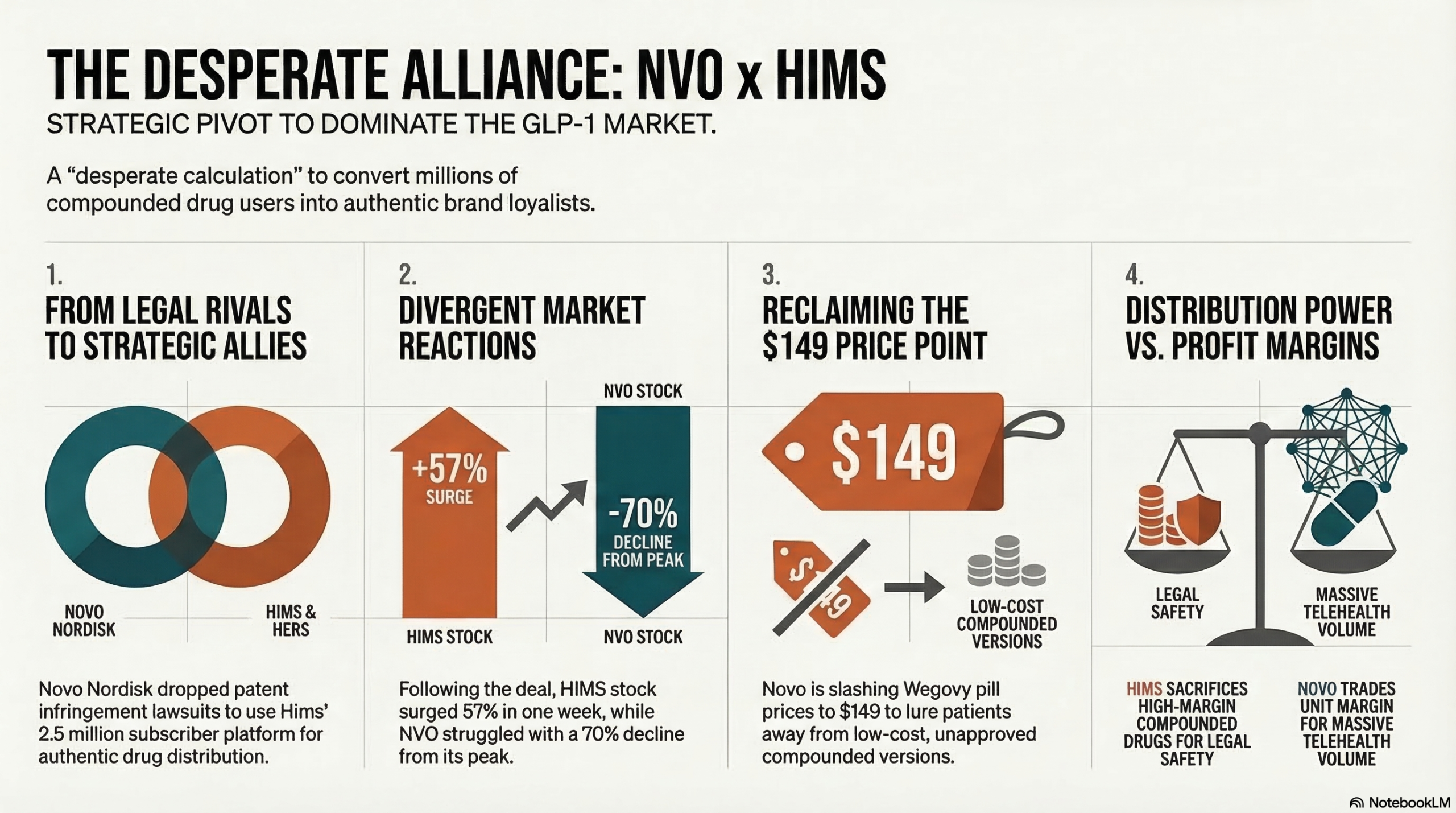

The market is currently cheering the partnership between Novo Nordisk (NVO) and Hims & Hers (HIMS) as a “new growth engine.” However, the actual ‘Delta’ in the data points in a completely different direction. Novo Nordisk’s stock remains stagnant near $38—a staggering 70% evaporation from its all-time high of $142—following a 2026 guidance shock delivered by management.

Conversely, while Hims & Hers celebrated a 57% surge immediately following the announcement, this is less an indicator of improved fundamentals and more a “Relief Rally” born from escaping a legal death sentence. This alliance is not a grand expansion; it is a desperate compromise between two entities backed into their respective corners. If investors remain blinded by Hims’ skyrocketing volume while ignoring Novo’s crumbling defenses, they risk falling into a fatal trap of information asymmetry.

[Fact] Novo Nordisk’s Crumbling Walls

Novo Nordisk’s 2026 guidance appears to be a “Kitchen Sink” strategy—an attempt to flush out every possible piece of bad news at once. Yet, the underlying figures confirm a structural crisis.

- Guidance Shock and Negative Growth: Novo shocked the market with a forecast of a 5–13% year-over-year decline in revenue and operating profit for 2026. In stark contrast to Eli Lilly’s (LLY) confident 25% growth projection, this represents an “innovation gap” now quantified in cold, hard numbers.

- Clinical Inferiority (KagriSema vs. Tirzepatide): The data showing that Novo’s counter-offensive card, KagriSema, is less effective than Lilly’s Tirzepatide was a decisive blow. Having lost ground in the next-gen race, Novo is now desperately pivoting toward Amycretin and MASH (Metabolic Dysfunction-Associated Steatohepatitis) indications to diversify its pipeline.

- A Self-Destructive Price War: The launch of oral Wegovy at a disruptive $149/month, combined with plans to slash list prices by 50% by 2027, is lethal to margins. While the volume is growing—capturing 170,000 prescriptions in just four weeks—the steep decline in unit price makes a short-term revenue hit inevitable.

Ultimately, Novo realized that a “Whack-a-Mole” legal strategy against over 100 small-scale compounders was a losing battle. Instead, they opted to “co-opt” Hims, the largest distribution network, to forcibly migrate over a million compounded-drug users back to authentic, branded products.

[Analysis] Hims & Hers: Escaping “Regulatory Arbitrage” for Legitimacy

HIMS’ 57% surge is not evidence of successful expansion. Until now, Hims relied on a “Regulatory Arbitrage” model, exploiting FDA shortage clauses to reap margins exceeding 80% on compounded GLP-1s. That model was destined to collapse the moment the shortage ended.

- Securing a “License to Exist”: Hims traded its 80% margins for a “legitimacy pass” through authorized distribution rights. The price for resolving the legal risks that weighed down its enterprise value is significant “Margin Dilution.”

- Fundamental Shift in Revenue Structure: Hims has been forcibly transitioned into a “Low-margin, High-volume” model. While the “Platform Lock-in” effect from converting 2.5 million subscribers to authentic products is a net positive, the explosive operating margins of the past are now a mirage.

- The “Ro” Factor and Platform Limitations: While some hail Hims as the “Amazon of Prescriptions,” we must not overlook that competitors like Ro were already distributing Wegovy and Zepbound. This deal is not a monopoly; it is a regression to the market mean.

Strategic Dashboard: Novo vs. Hims — Metrics Post-Alliance

| Category | Novo Nordisk (NVO) | Hims & Hers (HIMS) |

| Stock Performance | 70% drop from peak ($142 $\rightarrow$ $38) | 57% surge within one week of deal |

| 2026 Guidance | 5–13% Negative Growth (Revenue/Profit) | $2.7B Target (Growth vs. $2.3B in ’25) |

| Key Risks | Innovation gap with Lilly, Margin collapse | Dependence on Novo, Sharp margin contraction |

| Valuation | P/E 10x (Severely undervalued vs. 18x avg) | P/E 52x (Striving to maintain growth multiple) |

| Strategic Position | Co-opting networks to defend market share | Resolving legal risk & entering the mainstream |

| Notable Metric | Oral Wegovy $149 (170k scripts in 4 wks) | Trading volume surged 557% vs. 3-mo avg |

[Insight] Scenario Analysis & Counter-intuitive Outlook

Contrary to market optimism, the power of a pharmaceutical platform can vanish like a mirage the moment manufacturers decide to flex their “Direct-to-Consumer (DTC)” muscles.

[Scenario Planning]

- Best Case: Hims leverages its 2.5M subscribers to absorb Alzheimer’s and chronic disease medications, evolving into the dominant platform for U.S. healthcare accessibility.

- Worst Case: Novo throttles supply or re-exercises its legal rights, relegating Hims to a mere subcontracted distributor. The expansion of manufacturer-direct channels like “Novo Care” and “Lilly Direct” poses an existential threat to Hims.

[Counter-intuitive Insight: The Contrarian Opportunity] The real ‘Delta’ to watch is actually Novo’s valuation, which has crashed 70%. A P/E of 10x suggests the stock has reached a “Risk-Reward” equilibrium where all bearish factors are priced in. Conversely, Hims now faces the daunting task of defending its valuation amidst long-term margin erosion. This alliance granted Hims the “Right to Survive,” but it granted Novo the “Power to Control.”

3 Things Investors Must Verify Now

- Lilly’s Orforglipron Launch (Q2 2026): Monitor how much market share Lilly’s potent new oral drug steals from Novo, and whether Novo’s “Kitchen Sink” guidance truly represents the floor.

- HIMS Operating Margin Defense: Watch for a potential crash in margins to below 20% as they transition away from compounded drugs. Such a drop could shatter their growth multiple (P/E 52x).

- DTC Adoption Trends: Analyze the growth rate of Novo Care and Lilly Direct. Rapid adoption of these manufacturer-direct channels will quickly dilute the “intermediary value” of third-party platforms like Hims.

“Not a recommendation, just a shared strategic outlook. These are my personal reflections for collaborative study. Trade at your own discretion, share your unique views, and let’s grow together.”

Leave a Reply