Introduction: The ‘Silent Crisis’ of Stagnant Growth and Rising Inflation

The decoupling between Wall Street and the real economy is reaching a breaking point. U.S. Q4 GDP growth plummeted to 0.7%, less than half of the market’s 1.4% forecast, sending shockwaves through the financial sector. As consumer and government spending retreat, WTI has surged to $98.70, while Brent has already cleared the $100 resistance level for two consecutive days.

We are witnessing the “plumbing” of the market shake under the fear of stagflation. From a data analyst’s perspective, this isn’t just a correction—it’s a structural crack in liquidity. We must look behind the index to find the counterintuitive signals hidden in the noise.

Takeaway 1: Cracks in Private Credit and the ‘SaaS-pocalypse’

Private credit, the “shadow banking” titan that stepped in where traditional banks feared to tread, is showing signs of distress. This isn’t just sentiment; it’s a literal evaporation of capital.

- The Redemption Scream: BlackRock’s private funds fulfilled only 5% of a 9.3% redemption request, deferring the rest. Blackstone’s BCRED is facing a 7.9% withdrawal pressure, forcing the firm to tap into corporate cash and even personal funds from executives—an unprecedented move.

- The SaaS-pocalypse: The culprit is the deteriorating profitability of the software sector, which accounts for 20% of private credit exposure. As companies lose their interest coverage capacity, default rates spiked to 5.8% as of January 2026.

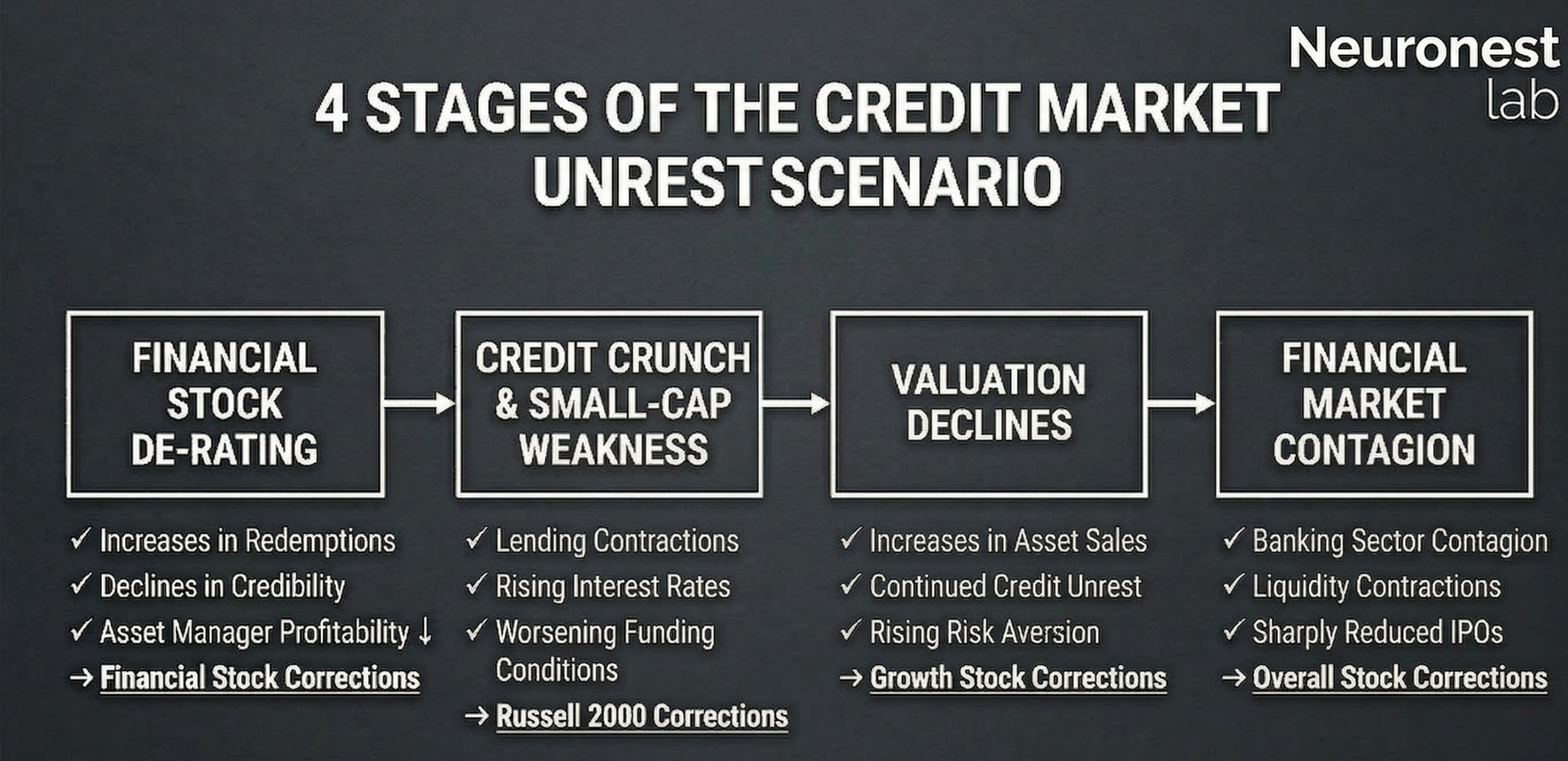

- The 4-Stage Crisis Path: We have passed Stage 1 (Financial De-rating) and are entering Stage 2 (Credit Crunch & Small-cap Weakness). Watch for valuation resets across all growth stocks (Stage 3) before potential contagion freezes the IPO market (Stage 4).

Takeaway 2: Is Rising Oil Bearish? The ’14th Red Dot’ in Historical Data

The myth that surging oil prices signal the end of a bull market dissolves when faced with data. Analyzing 13 instances since 1986 where WTI jumped over 5% in two days reveals a startling trend: Equities tend to rise regardless.

- The 85% Probability: During periods of rising oil, the S&P 500 has an 85% win rate, with an average annual return of 13.1%—outperforming periods of falling oil (11.3%).

- The 14th Red Dot: As of March 2026, we sit at the “14th Red Dot,” where oil has spiked 50% while the index remains flat. This is the watershed moment: will we follow the recovery models of 2002 and 2007, or the 2008 outlier?

- The Lesson: History suggests this fear is an 85% probability opportunity. However, a nuanced approach is required given the current growth slowdown.

Takeaway 3: Amazon’s Declaration of War: AI and Platform Sovereignty

Amazon’s move to block Perplexity AI’s shopping features is the opening salvo of a ‘Platform Sovereignty War.’ In a “SaaS-pocalypse” where software firms are struggling for credit, the winner-take-all structure favors platforms with massive cash flows.

- The Shift in Power: The traditional funnel (Search → Compare → Review → Buy) is collapsing into AI-driven “Recommend → Instant Checkout.” If AI controls the entry point, legacy platforms risk becoming mere delivery hubs.

- The Victory of Integration: The long-term winners won’t just have the best AI models; they will be the firms that vertically integrate AI platforms with dominant physical logistics.

Takeaway 4: SpaceX IPO: The ‘Liquidity Black Hole’ Threatening Big Tech

Rumors of a June IPO for Elon Musk’s SpaceX suggest a massive “Crowding Out” effect. This won’t bring new capital into the market; it will suck it out of existing leaders.

- Liquidity Migration: SpaceX is expected to debut as a top-6 global market cap entity. Investors are likely to sell Nvidia or Tesla to fund SpaceX positions, creating a massive supply-side headwind for current AI darlings.

- Nasdaq’s Fast-Track: To secure the listing, the Nasdaq is reportedly waiving its “6-month post-listing” rule for index inclusion.

- Timeline: Formalization in March, SEC filing in April, Roadshow in May, and a late June IPO. Growth investors must prepare for this rotation.

Takeaway 5: The Antifragility of U.S. ‘State-Level’ Economies

While a 0.7% national growth rate looks grim, the true strength of the U.S. lies in the sheer scale of its individual states.

- Global-Scale GDP: States like California, Texas, New York, and Florida possess GDPs comparable to G7 nations. California’s economy alone rivals major developed countries.

- The Case for Resilience: This decentralized, “country-sized” infrastructure provides Antifragility. While growth may stall, the structural hegemony of the U.S. economy remains intact. Doubting the system based on one quarterly number is premature.

Conclusion: Risks Don’t Vanish; They Migrate

As Jamie Dimon noted, “Risk doesn’t disappear; it just moves.” The market’s center of gravity has shifted from the AI bubble of 2024 to geopolitical tension, and now to oil prices and structural credit crunches.

As liquidity prepares to migrate from AI giants to SpaceX, and from private funds to safe-haven assets, where is your capital exposed? It is time to decide: will you bet on the historical 85% probability, or hedge for the 15% exception? For those who cannot read the path of migrating risk, the next bull market will be someone else’s celebration.

“Not a recommendation, just a shared strategic outlook. These are my personal reflections for collaborative study. Trade at your own discretion, share your unique views, and let’s grow together.”

Leave a Reply