-

The Gravity of $2 Trillion: Reshaping the Space Economy and Survival Strategies Triggered by the SpaceX IPO

Will the $2T SpaceX IPO be a re-valuation trigger or a liquidity vacuum? Explore structural shifts in the space sector and survival strategies for investors.

-

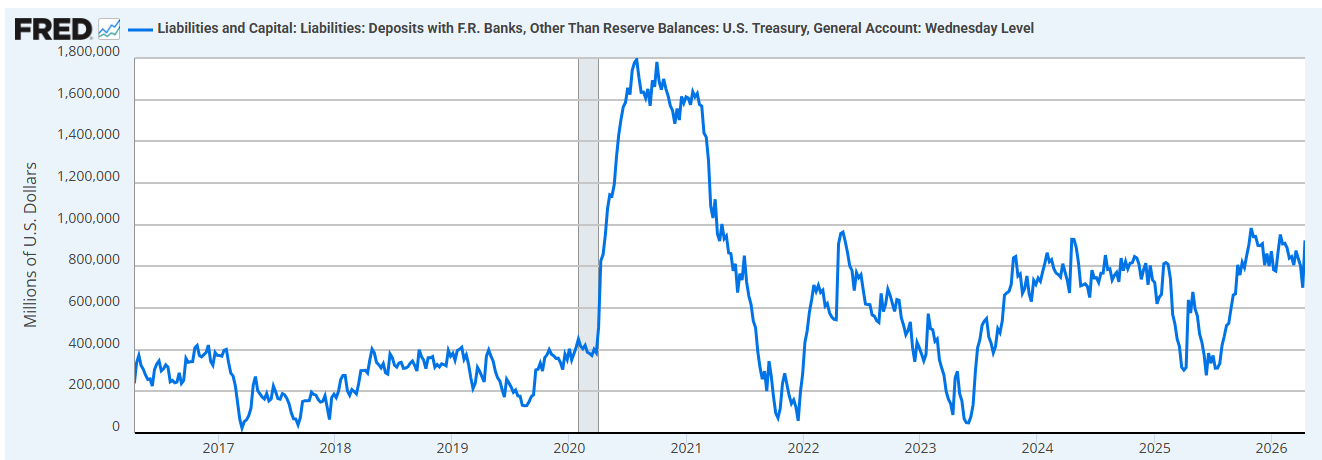

The Liquidity Spring: The Logic Behind Small Caps’ Pivot from ‘Laggards’ to ‘Leaders’

Analyzing the correlation between the Russell 2000 and Bitcoin amid a liquidity surge triggered by TGA drawdowns. Explore the investment strategies and earnings inflection points for key growth stocks like Tempus AI and IonQ.

-

The Index Betrayal: Why the S&P 500 Has Become Your Most Dangerous Asset

The myth of S&P 500 diversification is collapsing. Analyze the structural flaws of a market dominated by the 1.4% and discover 3 strategic shifts using RSP and SCHD to protect your portfolio.

-

The Great USB Revolt: Why SanDisk, Not HBM, is the Final Frontier of the AI Era

Is SanDisk (SNDK) the next NVIDIA? Explore why the structural NAND shortage and 625x AI inference demand make SanDisk the heart of AI infrastructure until 2028.

-

The ECB’s Dangerous Gamble: The Butterfly Effect of Diverging Monetary Policies in an Era of High Oil Prices

Explore why the ECB’s rate hike is a risky move compared to the Fed. Learn about supply shocks, oil prices, and the impact on global investments.

-

“Tesla isn’t a Car Company?”… 5 Contrarian Insights to Decide the Winner of the Energy War in the Data Center Era

Explore 5 contrarian insights on why Tesla is an energy titan, not just an EV maker, and how ESS will dominate the AI data center power market.

This is how it all started…

Wall Street is louder than ever, yet rarely clearer. Our mission is to bridge the gap between raw data and actionable intelligence, ensuring you never miss a signal in the sea of noise.

Ansel Junhyung Park

Writer & Journalist